A movement at an inflection point

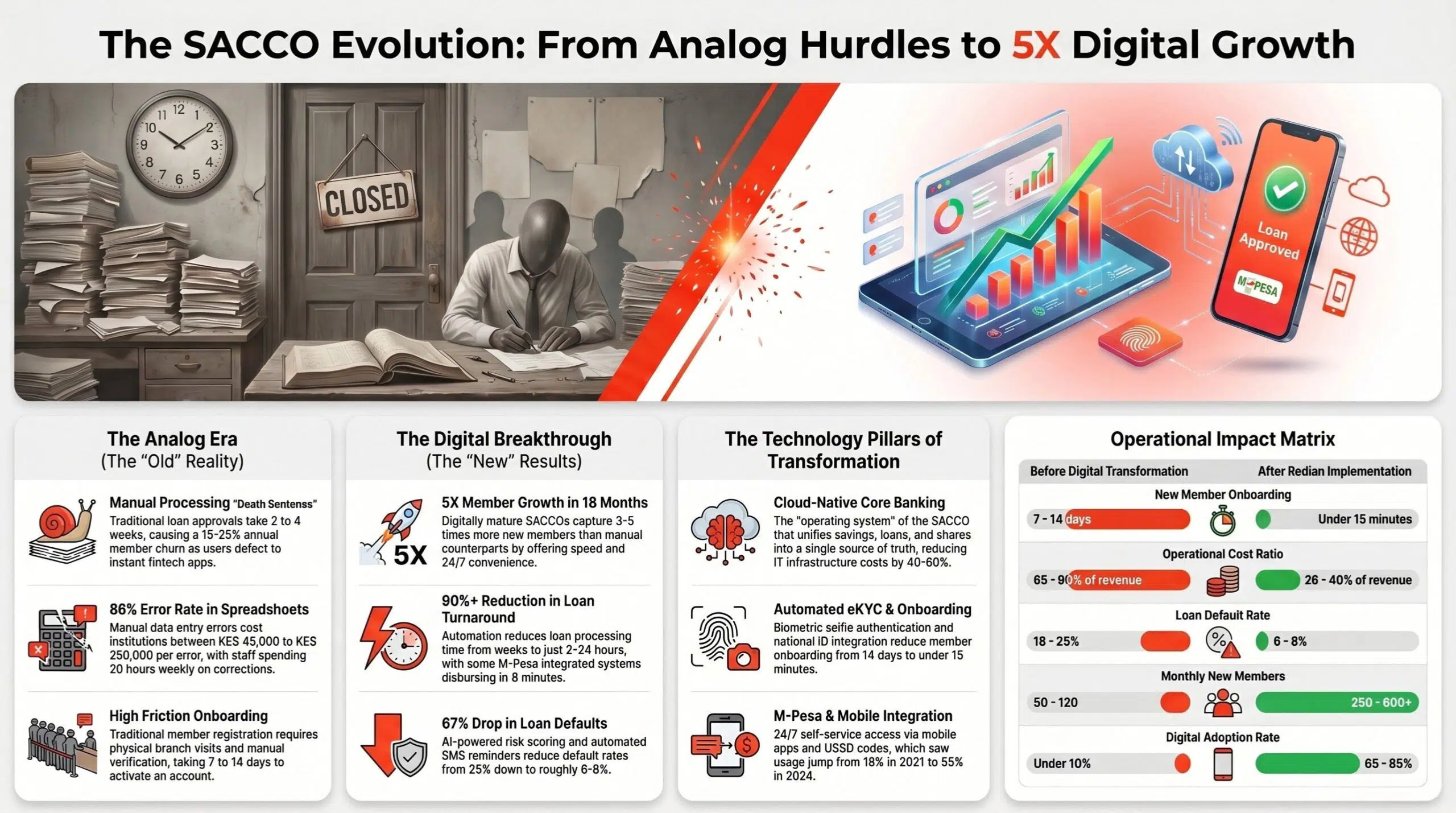

SACCOs are the backbone of financial inclusion across East and Southern Africa. From the dairy cooperatives of Kenya's Rift Valley to the matatu SACCOs of Nairobi and the agricultural unions of Tanzania and Cameroon, member-owned finance has done more to bank the unbanked than any commercial product. Yet many of these institutions still run on green-screen cores or hand-stitched workflows that cannot keep up with member expectations shaped by M-Pesa, Tigo Pesa and the broader fintech wave.

The gap between what members can do on their phone with a mobile-money wallet and what their SACCO can offer at the branch has become impossible to ignore. Regulators have noticed too — SASRA in Kenya, BoT in Tanzania, and BoU in Uganda have all tightened reporting cycles in ways that paper-and-spreadsheet operations simply cannot meet.

What digital core banking unlocks

- Member self-service — balance, deposits, withdrawals, loans, statements — without a branch visit.

- Faster loan origination — credit decisions in minutes, not weeks, using bureau pulls and rules-based scoring.

- Regulatory readiness — real-time reporting and audit trails the regulator will accept.

- Lower cost-to-serve — automation across the lifecycle of every product, from onboarding to closure.

The knock-on effect is growth. SACCOs that have digitised their core in the last 24 months are reporting member growth multiples that were unthinkable in the branch-only era — a pattern we explore in detail in our look atKenya's 5x credit union growth(/blog/sacco-management-system-credit-union-digital-transformation).

What to look for in a platform

- API-first architecture (not bolted on as an afterthought).

- Multi-currency, multi-product configuration without code changes.

- Mobile, USSD and agency channels included rather than sold separately.

- A vendor with delivery and support presence in your region — remote-only support models break down quickly when a branch in Mwanza or Bamenda needs a same-day fix.

How Redian helps

We operate core banking for SACCOs(/solutions/banking/core-banking) across Kenya, Uganda, Tanzania and Cameroon, with implementations typically delivered in 12 to 16 weeks including data migration from legacy systems. Our BFSI practice(/solutions/bfsi) wraps loan management, agency banking, mobile and USSD channels, and regulator reporting into a single integrated stack — so the SACCO doesn't carry the integration risk. For a closer look at past engagements, see our case studies(/case-studies) or get in touch(/contact) to scope a digitisation roadmap.

Stay current with our insights

One monthly email. Banking, insurance, AI/ML and CRM field notes. No spam.

We respect your privacy. Read our Privacy Policy.

Keep reading

More from Banking

Banking

SACCO management system — Kenya's credit unions achieve 5× member growth

How Kenya's credit unions are achieving 5× member growth in 18 months with digital-first SACCO management. The architecture, the playbook and the numbers.

28 May 2026

Banking

From Core Banking to Digital Channels: How Redian Software Empowers Financial Institutions in Cameroon

Redian Software empowers banks and microfinance institutions in Cameroon with core banking, loan management, mobile apps, USSD, and digital banking solutions.

30 Dec 2025

Banking

What Microfinance Institutions, NBFCs & Cooperatives in Southeast Asia Must Learn in 2025 — and How to Build a Winning Digital Strategy for 2026

Learn how microfinance institutions, NBFCs, and cooperatives in Indonesia, Vietnam, Malaysia, and the Philippines can build a scalable, compliant digital strategy for 2026.

26 Dec 2025

Build with Redian

Have a similar build in mind?

We've shipped banking systems for banks, insurers, brokers, MFIs, SACCOs and enterprises across the USA, UK, Africa, UAE and India. Book a 30-min call with a senior engineer — no pitch deck, just a sharp first read on your initiative.

- CMMI Level 3 Appraised · ISO Certified delivery

- 1 business day response · NDA on request

- Senior engineers, not sales — first call