What Microfinance Institutions, NBFCs & Cooperatives in Southeast Asia Must Learn in 2025 — and How to Build a Winning Digital Strategy for 2026

Learn how microfinance institutions, NBFCs, and cooperatives in Indonesia, Vietnam, Malaysia, and the Philippines can build a scalable, compliant digital strategy for 2026.

Across Southeast Asia, 2025 marked a clear inflection point for Microfinance Institutions (MFIs), NBFC-style lenders, cooperatives, and SACCOs. Customer expectations shifted decisively towardmobile-first, real-time, and transparent financial services, while regulators increasingly demanded responsible digital lending, stronger governance, and data privacy controls.

Institutions that invested early in digital platforms, alternative data, and ecosystem partnerships scaled faster and reduced operating costs. Those that delayed digital transformation faced rising acquisition costs, manual inefficiencies, and growing competitive pressure from fintechs and digital banks.

As we approach2026, the focus must move from experimentation to structured, scalable, and regulator-aligned digital strategy.

Mobile-First Is No Longer Optional

In Indonesia, Vietnam, Malaysia, and the Philippines, customers now expect lending and savings journeys that are:

Mobile-native

Simple and fast

Available anytime, anywhere

Institutions that redesigned journeys for mobile apps, assisted agents, and QR-based payments achieved:

Higher customer adoption

Faster loan disbursement

Improved repayment discipline

2025 insight: Digital channels must lead operations — not merely support branches.

Alternative Data Enabled Inclusive Growth

Traditional credit bureau data alone is insufficient for large segments of Southeast Asia’s population. In 2025, leading lenders successfully adopted:

Mobile wallet and QR transaction history

Merchant POS and agent-led transaction data

Utility, telco, and behavioral data

When combined with policy-driven controls and human review, alternative data improved credit access without increasing portfolio risk.

2026 mandate: Credit decisioning must be data-driven, explainable, and auditable.

Regulators Reward Responsible Digital Lenders

Regulatory frameworks across Southeast Asia increasingly emphasize:

Transparent pricing and disclosures

Affordability and indebtedness checks

Consumer consent and data protection

Ethical collections and hardship support

Institutions embedding responsible lending by design experienced smoother regulatory engagement and stronger customer trust.

Ecosystem Partnerships Drove Faster Scale

In 2025, the most successful growth strategies were built through:

Merchant and SME ecosystems

E-commerce and supply-chain platforms

Payroll-linked and cooperative networks

Distribution through partners outperformed standalone branch expansion.

At Redian Software, we work with MFIs, NBFCs, cooperatives, and financial institutions across emerging markets to:

Design mobile-first customer journeys

- Implement cloud-based core lending and payment platforms

- Enable alternative data–driven underwriting

- Ensure regulatory alignment and responsible lending

- Build API-based ecosystems and partnerships

Our experience across banking, insurance, fintech, and cooperative systems enables us to deliver solutions that are scalable, compliant, and commercially viable.

Customer Experience & Access

What leading institutions are building

Digital Onboarding & KYC

Onboarding completed in under 5 minutes, digitally or with agent support

Intelligent Lending & Data Platforms

Technology enhances — not replaces — credit governance.

Cloud-Native Core & Payments

Time-to-market and cost per loan.

Risk, Compliance & Governance

Strategic differentiators, not back-office functions.

Integrated mobile banking platform

Offers customers convenient 24/7 access to banking services.

Multi-lingual support

The system is fully translated into French, catering to the local market.

Stay current with our insights

One monthly email. Banking, insurance, AI/ML and CRM field notes. No spam.

We respect your privacy. Read our Privacy Policy.

Keep reading

More from Banking

Banking

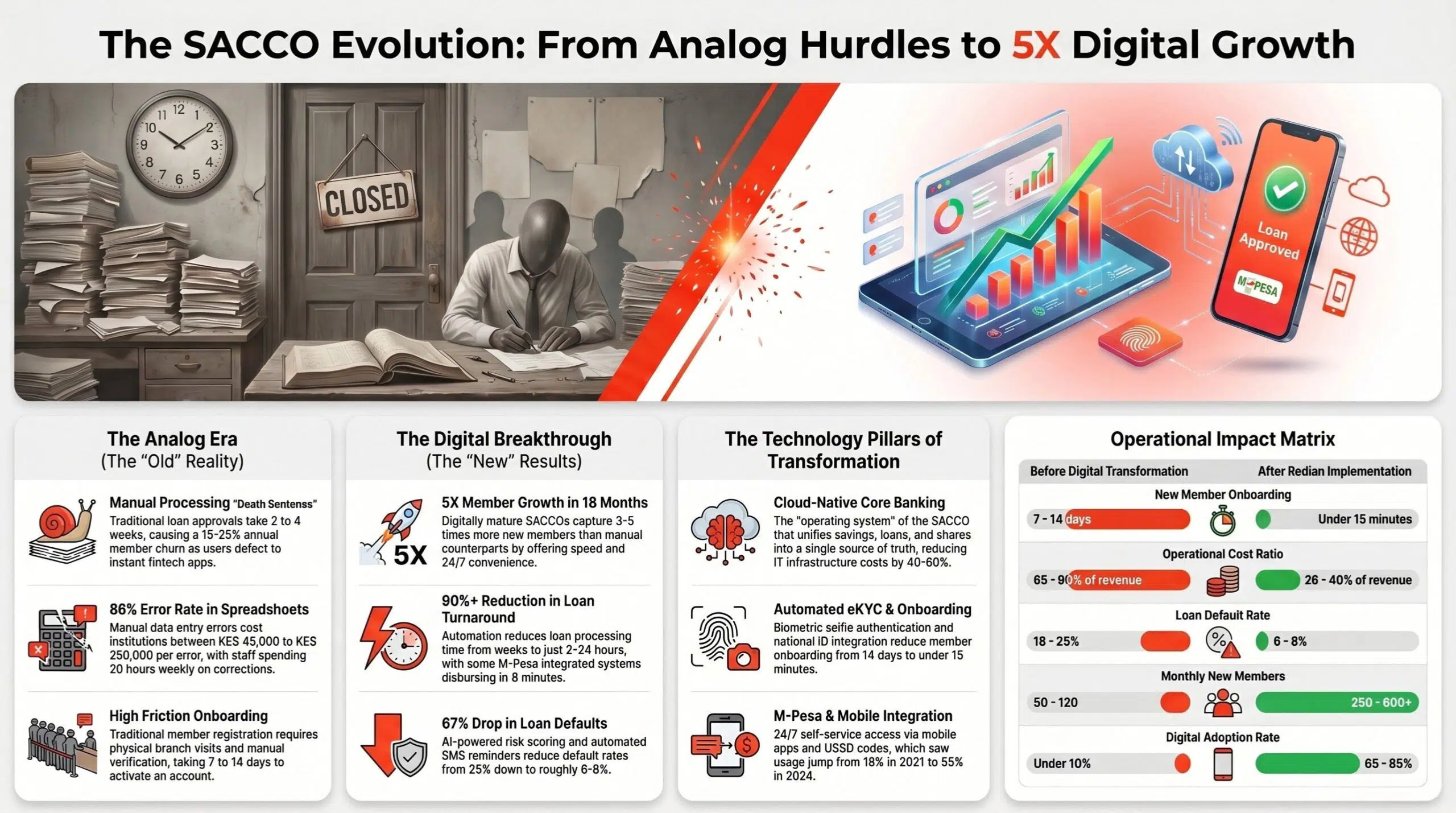

SACCO management system — Kenya's credit unions achieve 5× member growth

How Kenya's credit unions are achieving 5× member growth in 18 months with digital-first SACCO management. The architecture, the playbook and the numbers.

28 May 2026

Banking

Why SACCOs in Africa must adopt digital core banking — now

Member expectations have moved faster than legacy core systems. A practical case for digital core banking in the SACCO movement.

15 Apr 2026

Banking

From Core Banking to Digital Channels: How Redian Software Empowers Financial Institutions in Cameroon

Redian Software empowers banks and microfinance institutions in Cameroon with core banking, loan management, mobile apps, USSD, and digital banking solutions.

30 Dec 2025

Build with Redian

Have a similar build in mind?

We've shipped banking systems for banks, insurers, brokers, MFIs, SACCOs and enterprises across the USA, UK, Africa, UAE and India. Book a 30-min call with a senior engineer — no pitch deck, just a sharp first read on your initiative.

- CMMI Level 3 Appraised · ISO Certified delivery

- 1 business day response · NDA on request

- Senior engineers, not sales — first call