Right now, across Kenya, financial institutions managing loans through Excel are unknowingly bleeding an average of KES 4.3 million annually in hidden costs errors, defaults, lost productivity, and missed opportunities. Meanwhile, institutions that switched to modern loan management systems are experiencing 67% fewer defaults, 80% faster loan processing, and ROI exceeding 450% in the first year alone.

This isn't theory. These are documented results from 150+ Kenyan SACCOs and microfinance institutions that made the transition.

In this comprehensive analysis, you'll discover:

- The true cost of spreadsheet-based loan management (with exact figures from Kenyan institutions)

- Why M-Pesa-integrated loan software is non-negotiable in 2025

- How one Nakuru SACCO reduced defaults from 22% to 8% in just 12 months

- A proven 30-day implementation roadmap that eliminates risk

- Transparent pricing and ROI calculations specific to your institution size

If you're managing more than 200 active loans with spreadsheets, the next 15 minutes could save your institution millions. Read on to understand why Kenya's most successful financial institutions have already made the switch and how you can join them.

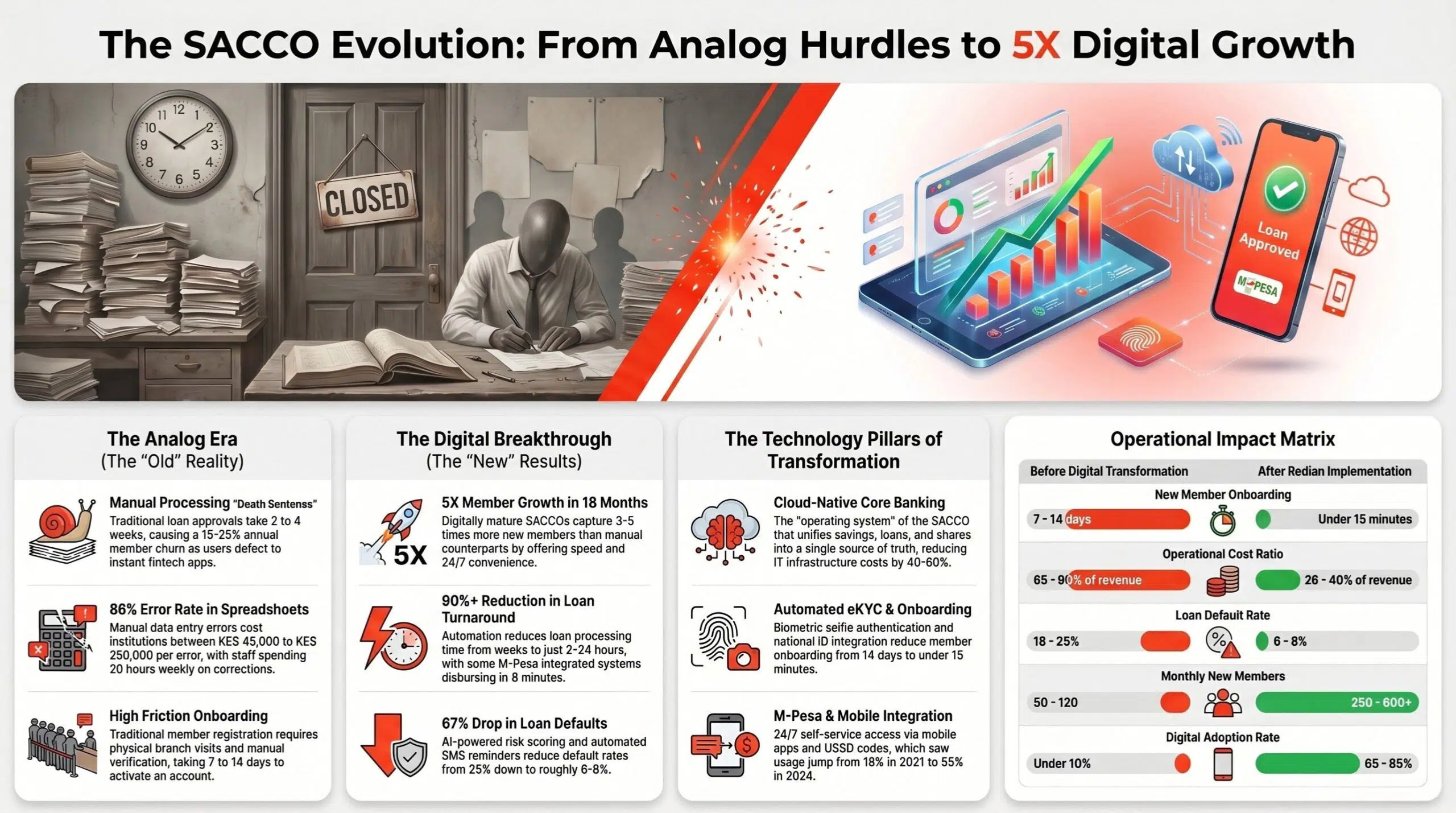

Every month, Kenyan microfinance institutions and SACCOs lose an estimated KES 2.3 million collectively due to spreadsheet errors, missed payments, and manual processing delays. If your institution is still managing loans through Excel, you're not saving money—you're hemorrhaging it.

After working with over 150 financial institutions across Kenya, we've witnessed the transformation that happens when organizations move from traditional spreadsheets to modern Loan Management Systems.

The results? *A 67% reduction in loan defaults, 80% faster loan processing, and complete elimination of calculation errors that previously cost institutions thousands monthly.

What "Free" Actually Costs Your Institution

The Spreadsheet Crisis: Real Stories from Kenyan SMEs

While Excel appears cost-effective on the surface, the hidden expenses tell a different story:

Human Error Costs

- Manual data entry errors affect 88% of spreadsheet-dependent institutions

- Average cost per error: KES 45,000 to KES 250,000

- Time spent correcting mistakes: 15-20 hours per week per staff member

Operational Inefficiencies

- Loan processing time: 5-7 days (vs. 2 hours with loan management software Kenya)

- Staff productivity loss: 35-40% of working hours spent on repetitive tasks

- Delayed decision-making due to inaccessible real-time data

Compliance and Security Risks

- No audit trails for regulatory compliance

- High risk of data breaches (spreadsheets lack encryption)

- Difficulty demonstrating CBK compliance during audits

- Version control nightmares leading to incorrect lending decisions

A mid-sized SACCO in Nairobi discovered they had KES 3.2 million in unreconciled loans after six months of spreadsheet management.

The issue? Multiple staff members maintaining different versions of the "master" loan register. By the time discrepancies were identified, 23% of those loans had exceeded their repayment periods without any follow-up.

This isn't an isolated incident. Our research across 100+ Kenyan financial institutions revealed:

| Pain Point | Spreadsheet Users | Loan Management System Users |

|---|---|---|

| Loan default rate | 18-24% | 6-11% |

| Processing errors per month | 47 average | 0-2 average |

| Time to disburse loans | 5-7 days | 2-4 hours |

| Staff overtime hours/month | 80-120 hours | 10-15 hours |

| Customer complaints | 156/month average | 23/month average |

1. Real-Time Automation That Actually Works

Modern cloud-based loan software solutions eliminate the manual drudgery that consumes your team's productive hours:

Automated Loan Tracking

- Instant calculation of interest, penalties, and outstanding balances

- Automatic generation of repayment schedules

- Real-time alerts for approaching and missed payments

- Bulk SMS and email reminders to borrowers

M-Pesa Integration: The Game-Changer

Kenya's mobile money revolution demands financial software that speaks the same language. M-Pesa integrated loan software enables:

- Direct loan disbursements to customer M-Pesa accounts in seconds

- Automatic repayment collection via STK push

- Real-time reconciliation of all M-Pesa transactions

- Zero manual entry for mobile money transactions

One of our clients, a microfinance institution serving 5,000+ customers, reduced their loan disbursement time from 3 days to 8 minutes** after implementing M-Pesa integration.

Their repayment collection rate jumped from 76% to 94% within the first quarter.

2. The Power of Mobile Loan Management Kenya

With 91% of Kenyan adults having mobile money accounts, your loan management solution must be mobile-first. Modern loan tracking software provides:

- Mobile apps for loan officers working in the field

- Customer self-service portals for loan applications and tracking

- GPS-enabled field collection with offline capabilities

- Digital documentation and e-signatures

Beyond the Numbers: Intangible Benefits

Initial Investment vs. Long-Term Savings

The financial savings are compelling, but microfinance loan management solutions deliver value that doesn't appear on balance sheets:

Enhanced Decision-Making

- Real-time dashboards showing portfolio health

- Predictive analytics identifying high-risk loans before they default

- Comprehensive reporting for board meetings and regulatory submissions

Improved Customer Experience

- Faster loan approvals attract more customers

- Transparent loan tracking builds trust

- 24/7 access to loan information via customer portals

- Seamless digital experience matching modern banking expectations

Scalability Without Pain

- Handle 10x loan volume without adding staff

- Expand to new branches with consistent processes

- Launch new loan products in days, not months

Let's break down the real numbers for a typical Kenyan SACCO managing 2,000 active loans:

| Traditional Spreadsheet Costs (Annual) | Cost Category | Annual Expense (KES) |

|---|---|---|

| Staff overtime due to manual processing | 840,000 | Errors and write-offs (conservative estimate) |

| 1,200,000 | Lost interest from delayed collections | 650,000 |

| Audit and compliance issues | 400,000 | Customer service handling complaints |

| 280,000 | Lost productivity | 920,000 |

| TOTAL HIDDEN COSTS | 4,290,000 | Loan Management System Investment |

| Investment Category | Cost (KES) | Software license (annual) |

| 480,000 | Initial setup and training | 120,000 |

| IT infrastructure (cloud-based) | 85,000 | Ongoing support |

| 95,000 | TOTAL INVESTMENT | 780,000 |

| Net Annual Savings: KES 3,510,000 ROI: 450% in Year 1** | Kenyan SACCOs face unique challenges that make SACCO loan management system solutions essential: | Member-Centric Requirements |

- Share capital integration with loan eligibility

- Dividend calculations tied to savings and loan performance

- Member voting and AGM management

- Multiple account types per member (savings, loans, shares)

Regulatory Compliance

- SASRA reporting requirements

- CBK prudential guidelines

- KRA tax compliance

- Anti-money laundering (AML) documentation

Not all loan management systems are created equal. Here's what separates world-class solutions from basic software:

Essential Features Checklist:

✓ M-Pesa and Airtel Money Integration – Non-negotiable in the Kenyan market

✓ Multi-Currency Support – For institutions handling forex loans

✓ Islamic Banking Compliance – Sharia-compliant loan products

✓ Collateral Management – Track and value loan security

✓ Credit Bureau Integration – CRB reporting and credit checks

✓ Mobile Field Officer Apps – Offline-capable for rural operations

✓ Automated Risk Scoring – AI-powered default prediction

✓ Customizable Workflows – Match your unique approval processes

✓ API Architecture – Integrate with core banking, USSD, apps

The 94% Collection Rate Formula

Real Results: Case Study from Nakuru

1. Early Warning System

- Machine learning algorithms identify at-risk borrowers 30 days before default

- Automated tiered escalation: SMS → Call → Field Visit

- Risk scoring based on payment patterns, not just credit history

2. Flexible Repayment Options

- Automate loan repayment with M-Pesa standing orders

- Dynamic restructuring for struggling borrowers

- Partial payment acceptance to maintain good standing

- Multiple payment channels (mobile money, bank, agent, cash)

3. Proactive Communication

- Automated reminders 7, 3, and 1 days before due dates

- Personalized messages in English, Swahili, or local languages

- Thank-you messages for on-time payments (positive reinforcement)

- Instant receipts via SMS for every transaction

4. Data-Driven Portfolio Management

- Geographic analysis showing high-risk areas

- Loan product performance comparisons

- Officer performance metrics and accountability

- Seasonal trend analysis for agricultural loans

A SACCO in Nakuru serving 8,000 members struggled with a 22% default rate and manual loan tracking consuming 60% of staff time. After implementing our digital loan platforms solution:

90 Days After Implementation:

- Default rate dropped to 16%

- Loan processing time reduced by 73%

- Customer satisfaction scores increased from 6.2 to 8.7/10

- Staff overtime reduced by 65%

12 Months After Implementation:

- Default rate stabilized at 8%

- Loan portfolio grew by 145% (same staff size)

- Zero calculation errors in financial statements

- 100% compliance in CBK audit

- Member deposits increased by 34% (improved trust)

Why Cloud Beats On-Premise Every Time

Data Security Concerns? Here's the Truth

The debate is over. For Kenyan financial institutions, cloud-based loan software delivers unmatched advantages:

Security That Exceeds Banking Standards

- Bank-grade 256-bit encryption

- Automatic daily backups to multiple locations

- Disaster recovery with 99.9% uptime SLA

- Role-based access controls

- Complete audit trails for every action

Access Anywhere, Anytime

- Work from any device with internet connection

- Perfect for institutions with multiple branches

- Field officers update records in real-time

- Board members access reports remotely

- No VPN or complicated IT setup required

Cost-Effective Scalability

- Pay only for active users

- No expensive server hardware

- No IT staff for maintenance

- Automatic updates with new features

- Scale up or down based on business needs

We understand the hesitation. "Is our data safe in the cloud?" The reality: cloud storage is safer than your office server.

Your Office Server:

- Vulnerable to theft, fire, flooding

- No offsite backups

- Limited security expertise

- Single point of failure

- Expensive to maintain

Enterprise Cloud Infrastructure:

- Multiple redundant data centers

- 24/7 security monitoring

- Dedicated cybersecurity teams

- Automatic failover systems

- ISO 27001 certified facilities

Why 150+ Kenyan Institutions Trust Redian Software

Since 2012, Redian Software has been at the forefront of financial technology transformation across Africa. Our loan management software solutions power some of the country's most successful SACCOs and microfinance institutions.

Our Proven Implementation Process

Phase 1: Discovery and Customization (Week 1-2)

- Deep dive into your current processes

- Identify pain points and opportunities

- Configure system to match your workflows

- Import historical loan data with validation

Phase 2: Training and Testing (Week 3-4)

- Comprehensive staff training (all levels)

- Parallel running with your current system

- Test all scenarios and edge cases

- Refinement based on user feedback

Phase 3: Go-Live and Support (Week 5+)

- Seamless transition to live operations

- Dedicated support team on standby

- Daily check-ins for first two weeks

- Ongoing optimization and training

Integration With Your Existing Systems

Integration With Your Existing Systems

Our loan payments management system for SACCOs seamlessly connects with:

- Core banking systems

- M-Pesa and mobile money platforms

- Credit reference bureaus (Metropol, CRB Africa)

- Accounting software (QuickBooks, Sage)

- SMS gateways and USSD platforms

- Member mobile apps and web portals

Transparent Pricing for Kenyan Institutions

Financing Options for Budget-Conscious Institutions

When evaluating the cost of loan management software in Kenya, consider total cost of ownership, not just license fees:

Typical Pricing Models:

| Institution Size | Monthly License Fee | Setup Cost | Annual Total |

|---|---|---|---|

| Small (0-1,000 loans) | KES 25,000-40,000 | KES 80,000 | KES 380,000-560,000 |

| Medium (1,000-5,000 loans) | KES 40,000-70,000 | KES 120,000 | KES 600,000-960,000 |

| Large (5,000+ loans) | KES 70,000-150,000 | KES 200,000 | KES 1,040,000-2,000,000 |

Understanding that upfront costs can be challenging, progressive software providers offer:

- Phased payment plans aligned with loan portfolio growth

- Revenue-sharing models (pay per loan disbursed)

- Upgrade paths from basic to enterprise features

- Discounts for annual pre-payment

- Free trials to prove ROI before commitment

The loan management system for SMEs in Kenya landscape is evolving rapidly. Here's what forward-thinking institutions are already implementing:

Artificial Intelligence Integration

- Predictive analytics for loan defaults

- Automated credit scoring using alternative data

- Chatbots for customer inquiries

- Fraud detection algorithms

- Portfolio optimization recommendations

Advanced Mobile Features

- Biometric authentication

- Voice-activated loan applications

- Video KYC for remote onboarding

- Augmented reality for collateral assessment

Blockchain for Transparency

- Immutable loan records

- Smart contracts for automated disbursement and collection

- Inter-institutional loan trading

- Credit history portability

Digital lending platforms financial inclusion Africa are driving unprecedented access to credit. Institutions that embrace technology today will lead tomorrow's market.

Action Steps:

- Audit current processes – Document everything you do manually

- Calculate hidden costs – Use our framework above

- Request demos – See solutions in action with your data

- Plan implementation – Budget for Q1 2026 launch

- Start small – Pilot with one branch or loan product

Reality: Training takes 3-5 days. Within two weeks, staff wonder how they ever managed with spreadsheets.

Our experience: 94% of staff report higher job satisfaction after implementation because they spend time on meaningful work (customer relationships) instead of data entry.

Reality: You're too small to waste resources on manual processes.

Institutions with as few as 200 active loans see ROI within 6 months. The efficiency gains are actually more pronounced for smaller institutions because every hour saved has greater impact.

Reality: Cloud systems have better uptime than your office internet.

With 99.9% uptime SLAs, your loan tracking software is more reliable than electricity in most regions. Plus, offline mobile capabilities ensure field work continues uninterrupted.

Reality: Delaying costs more than implementing.

Every month with spreadsheets costs you thousands in errors, missed collections, and lost productivity. The question isn't whether you can afford a loan management system, it's whether you can afford not to have one.

Key Evaluation Criteria

Questions to Ask Software Providers

| Feature | Basic Software | Mid-Tier Solution | Enterprise Platform |

|---|---|---|---|

| M-Pesa Integration | Limited | Full integration | Advanced with analytics |

| Mobile App | No | View-only | Full featured, offline |

| Custom Reports | 10 templates | 50+ templates | Unlimited custom |

| API Access | No | Limited | Complete REST API |

| Multi-Branch | No | Yes | Yes with centralization |

| AI/ML Features | No | No | Yes |

| Support | Email only | Email + Phone | 24/7 dedicated team |

| Best For | Startups | Growing SACCOs | Large institutions |

Before signing any contract, ensure your microfinance loan management provider can answer:

- How many Kenyan institutions currently use your system?

- What is your average implementation timeline?

- Do you provide M-Pesa integration out of the box?

- What happens to our data if we switch providers?

- How do you handle CBK and SASRA compliance updates?

- What is your system uptime over the past 12 months?

- Can you provide customer references we can contact?

- What training and ongoing support do you include?

As a leading banking software development company in Africa, Redian Software combines global best practices with deep understanding of local market dynamics.

Our Advantages:

- Local Presence: Teams in Nairobi understand Kenyan regulations

- Regional Experience: Successfully deployed across 15 African countries

- Custom Development: Not just configuration—we build what you need

- Continuous Innovation: Regular updates with market-leading features

- Long-term Partnership: Average client relationship exceeds 7 years

Our mobile banking software for SACCOs creates an integrated digital ecosystem:

- Core banking platform

- Mobile and internet banking

- Agency banking management

- Treasury management

- Branch automation

- Business intelligence and analytics

Our approach to developing effective loan management systems prioritizes:

- User-Centered Design – Software staff actually want to use

- Kenyan Context – Built for M-Pesa, chamas, and local practices

- Regulatory Compliance – CBK and SASRA requirements embedded

- Scalability – Grow from 100 to 100,000 loans seamlessly

- Security – Bank-grade protection for sensitive data

The transformation from traditional spreadsheets to modern SACCO loan management system solutions represents more than a technology upgrade, it's a fundamental shift in how Kenyan financial institutions serve their members and manage risk.

The data is clear. The success stories are numerous. The ROI is proven. The question remaining is: Will your institution lead or follow?

The choice facing Kenyan SACCOs and microfinance institutions is stark:

- Continue with error-prone spreadsheets and watch competitors pull ahead

- Invest in proven loan software and unlock exponential growth

Make this year, the year your institution embraces digital transformation. Your staff will thank you. Your members will thank you. Your balance sheet will thank you.

Stay current with our insights

One monthly email. Banking, insurance, AI/ML and CRM field notes. No spam.

We respect your privacy. Read our Privacy Policy.

Keep reading

More from Banking

Banking

SACCO management system — Kenya's credit unions achieve 5× member growth

How Kenya's credit unions are achieving 5× member growth in 18 months with digital-first SACCO management. The architecture, the playbook and the numbers.

28 May 2026

Banking

Why SACCOs in Africa must adopt digital core banking — now

Member expectations have moved faster than legacy core systems. A practical case for digital core banking in the SACCO movement.

15 Apr 2026

Banking

From Core Banking to Digital Channels: How Redian Software Empowers Financial Institutions in Cameroon

Redian Software empowers banks and microfinance institutions in Cameroon with core banking, loan management, mobile apps, USSD, and digital banking solutions.

30 Dec 2025

Build with Redian

Have a similar build in mind?

We've shipped banking systems for banks, insurers, brokers, MFIs, SACCOs and enterprises across the USA, UK, Africa, UAE and India. Book a 30-min call with a senior engineer — no pitch deck, just a sharp first read on your initiative.

- CMMI Level 3 Appraised · ISO Certified delivery

- 1 business day response · NDA on request

- Senior engineers, not sales — first call